Lee Heidhues 3.10.2023

Bank failures are akin to a tsunami in the financial world.

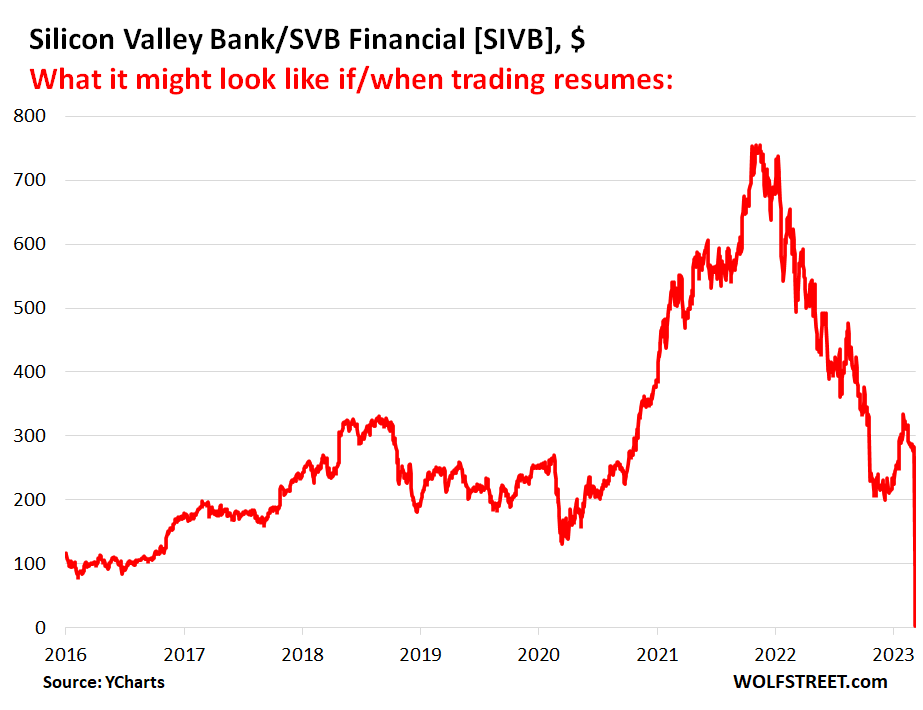

The collapse of Silicon Valley Bank is a world wide story receiving major headline coverage.

The collapse of this bank, 16th largest in the United States, holds particular relevancy in the Bay Area.

The Standard, an online publication in San Francisco, was founded by prominent venture capitalists. Its current online edition has eight stories about the collapse of SVB. https://sfstandard.com/ A lead story being headlined ‘Bay Area Investors Clamor for Government to Step up After Silicon Valley Bank Meltdown.’

The Wall Street Journal is playing the story across the front page of its online edition. The last sentence in the editorial is the most telling about what America’s leading financial publication is really thinking.

But nobody, least of all central bank oracles, should be surprised that there are now bodies washing up on shore as the tide goes out. Investors will have to brace for what could be some heavy weather ahead.

Following is the WSJ editorial.

Wall Street Journal editorial 3.10.2023

There’s nothing like a bank panic to make for a relaxing weekend.

Markets took another header on Friday, as regulators closed Silicon Valley Bank (SVB), the 16th largest U.S. bank and the biggest to fail since the 2008 crisis. This came days after Silvergate Capital announced it is liquidating its bank. Cracks in the financial system emerge whenever interest rates rise quickly after an easy-credit mania, and the surprise is that it took so long.

The Federal Deposit Insurance Corporation took over SVB on Friday and may have to collect more bodies by the time the Federal Reserve is done correcting its easy-money mistakes. At least that seems to be the fear of investors, judging by the sharp selloff in regional bank stocks like First Republic Bank (-14.8%) and PacWest Bancorp (-37.9%).

SVB’s customers include leading venture-capital firms and tech startups, including some Chinese firms that need offshore accounts to raise foreign capital. San Diego-based Silvergate is smaller but grew in recent years by serving crypto companies.

What the two have in common is that they lacked diverse deposit bases and fell victim of a classic banking strategy of borrowing short and lending long. Although their liabilities were backed by putatively safe assets like Treasury bonds, when interest rates rise the bonds that banks hold lose value. They have to be held to maturity or incur losses when sold.

SVB and Silvergate incurred steep losses as they sold bonds to compensate for fleeing deposits. A regulatory crackdown on crypto also spurred Silvergate customers to bail, sticking it with even bigger losses.

Silvergate on Wednesday said it would liquidate “in light of recent industry and regulatory developments.” Its crypto ties may have made it too politically toxic for another bank to take over. While regulators will surely flog Silvergate’s failure as a warning not to serve the crypto industry, its concentrated deposit base was the main cause of its demise.

SVB’s business model was more durable but still vulnerable to market shocks. Rising interest rates have made it hard for its startup clients to raise fresh equity. As its customers drew down deposits, SVB had to sell bonds at a loss. SVB disclosed this week that it had lost $1.8 billion on securities sales and would need to raise $2.25 billion in equity.

This stoked fears of insolvency, which caused customers and investors to bolt. It was reportedly searching for a buyer on Friday, and we hope regulators didn’t pre-empt potential private investors by closing SVB so quickly on the same day.

Bank of America and J.P. Morgan rescued smaller banks during the 2008 crisis. But banks may be reluctant to do that again since regulators last time punished them for the sins of their foster children. The takeover of SVB will presumably cost the FDIC money to repay insured depositors.

But if SVB was doomed, it is better to let it fail than have the government bail it out, despite what one hedge-fund lord suggested this week. Didn’t we learn from the 2008 crisis that the feds’ rescue of Bear Stearns encouraged everyone to believe that Lehman Brothers would be rescued too?

There doesn’t appear to be any obvious systemic risk to the financial system from the SVB and Silvergate failures, and market discipline needs to prevail unless there is danger of a larger financial breakdown. SVB investors and customers benefited from the government’s easy money. Why should they also benefit from a government lifeline after taking risks with that easy money?

This week’s bank failures are another painful lesson in the costs of a credit mania fed by bad monetary policy. The reckoning always arrives when the Fed has to correct its mistakes. That was the story of 2008, and it’s the eternal lesson that economic historian Charles Kindleberger taught in “Manias, Panics, and Crashes.” We saw the first signs of panic in last year’s crypto crash and the liquidity squeeze at British pension funds.

Now it’s hit the U.S. financial system, and there are likely to be more casualties. Treasury Secretary Janet Yellen said Friday that the U.S. banking system “remains resilient,” but that’s what Fed officials Ben Bernanke and Tim Geithner thought before the 2008 panic.

While big banks today are much better capitalized than before the 2008 financial crisis, some regional and small banks with less diverse deposit bases may be vulnerable to shocks. Some may be over-exposed to industries such as commercial real estate that are under stress. The Fed will have to be careful as it continues its anti-inflation campaign.

But nobody, least of all central bank oracles, should be surprised that there are now bodies washing up on shore as the tide goes out. Investors will have to brace for what could be some heavy weather ahead.